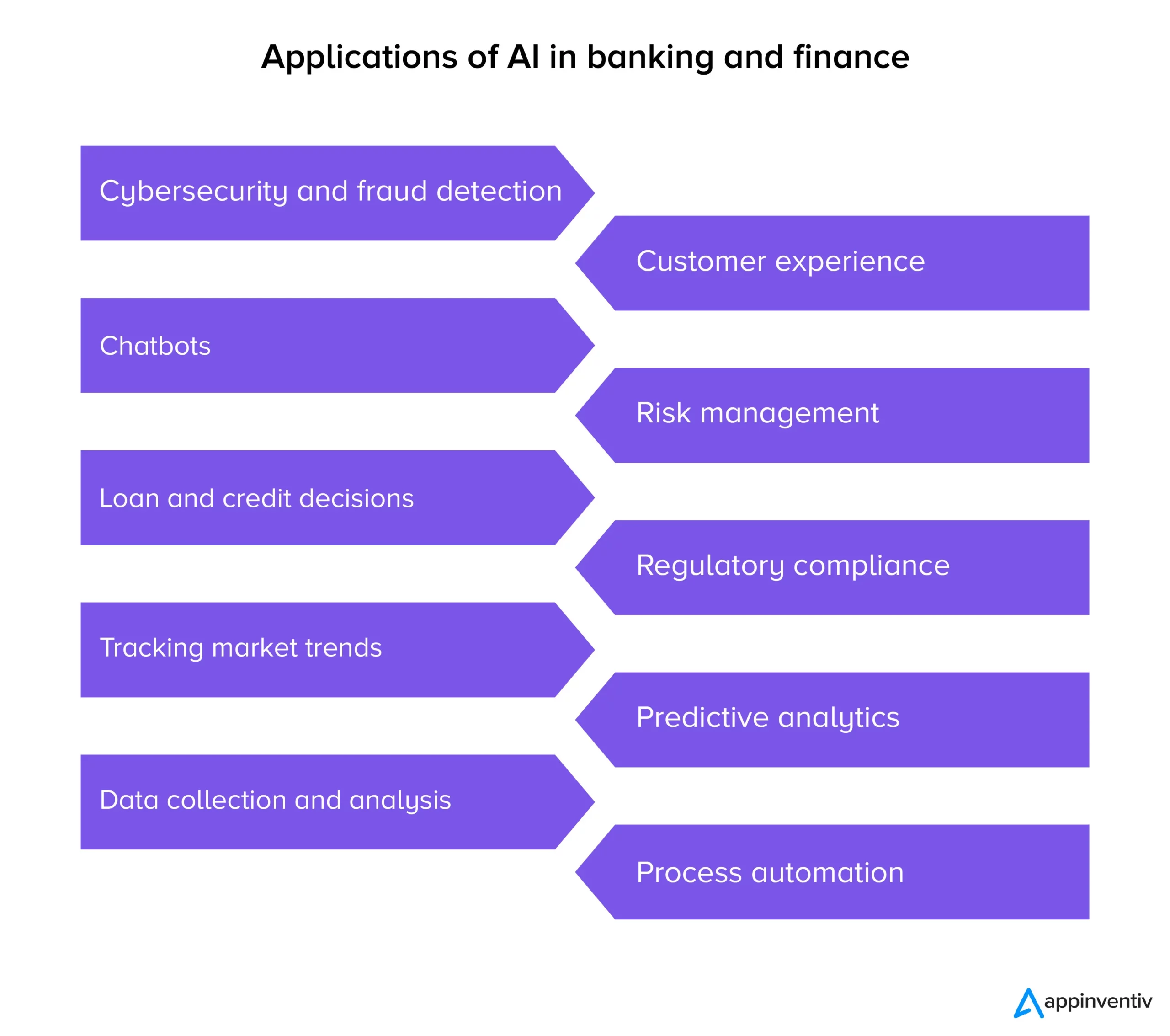

- Applications of AI in Banking and Finance

- Cybersecurity and Fraud Detection

- Chatbots

- Loan and Credit Decisions

- Tracking Market Trends

- Data Collection and Analysis

- Customer Experience

- Risk Management

- Regulatory Compliance

- Predictive Analytics

- Process Automation

- Real-World Examples of AI in Banking

- Challenges in Adopting AI & ML in Banking

- Data Security

- Lack of Quality Data

- Lack of Explainability

- Why Must the Banking Sector Embrace the AI-First World?

- The Generative AI Impact

- Steps to Become an AI-First Bank

- Step 1: Develop an AI Strategy

- Step 2: Plan a Use Case-Driven Process

- Step 3: Develop and Deploy

- Step 4: Operate and Monitor

- How Appinventiv Can Help in Your AI for Banking Journey

- FAQs

- Q. How does AI help in Banking?

- Q. How AI helps in banking risk management?

- Q. Which are the most important Generative AI use cases in banking?

- Q. What are the top AI trends in banking?

AI’s transformative impact has been profound since its advent, changing how enterprises, including those in the banking and finance sector, operate and deliver services to customers. The introduction of AI in banking apps and services has made the sector more customer-centric and technologically relevant.

AI-based systems are now helping banks reduce costs by increasing productivity and making decisions based on information unfathomable to a human. Also, intelligent algorithms can spot fraudulent information in a matter of seconds.

A report by Business Insider suggests that nearly 80% of banks are aware of the potential benefits of AI in banking. Another report by McKinsey suggests the potential of AI in banking and finance would grow as high as $1 trillion.

These numbers indicate that the banking and finance sector is swiftly moving towards AI to improve efficiency, service, and productivity and reduce costs.

In this blog, we will discover the key applications of AI in the banking and finance sector and will also look at how this technology is redefining customer experience with its exceptional benefits.

Applications of AI in Banking and Finance

Artificial intelligence has become an integral part of our world, and banks have already started integrating this technology into their products and services. Here are some major AI applications in the banking industry:

Cybersecurity and Fraud Detection

Several digital transactions occur daily as users pay bills, withdraw money, deposit checks, and do much more via apps or online accounts. Thus, there is an increasing need for the banking sector to ramp up its fraud detection efforts.

This is when artificial intelligence in banking comes to play. AI and machine learning helps banks identify fraudulent activities, track loopholes in their systems, minimize risks, and improve the overall security of online finance.

One such example of a bank using AI for fraud detection includes Danske Bank, which is Denmark’s largest bank to implement a fraud detection algorithm in its business. The deep learning tool increased the bank’s fraud detection capability by 50% and reduced false positives by 60%. The AI-based fraud detection system also automated a lot of crucial decisions while routing some cases to human analysts for further inspection.

AI can also help banks to manage cyber threats. In 2019 the financial sector accounted for 29% of all cyber attacks, making it the most-targeted industry. With the continuous monitoring capabilities of artificial intelligence in financial services, banks can respond to potential cyberattacks before they affect employees, customers, or internal systems.

Chatbots

Chatbots are one of the best examples of practical applications of artificial intelligence in banking. Once deployed, they work 24*7, unlike humans with fixed working hours.

Additionally, they keep learning about a particular customer’s usage pattern. It helps them understand the requirements of a user efficiently.

By integrating chatbots into banking apps, banks can ensure they are available for their customers around the clock. Moreover, by understanding customer behavior, chatbots can offer personalized customer support reduce workload on emailing and other channels, and recommend suitable financial services and products.

One of the best examples of AI chatbots for banking apps is Erica, a virtual assistant from the Bank of America. The AI chatbot handles credit card debt reduction and card security updates efficiently, which led Erica to manage over 50 million client requests in 2019.

Loan and Credit Decisions

Banks have started incorporating AI-based systems to make more informed, safer, and profitable loan and credit decisions. Currently, many banks are still too confined to the use of credit history, credit scores, and customer references to determine the creditworthiness of an individual or company.

However, one cannot deny that these credit reporting systems are often riddled with errors, missing real-world transaction history, and misclassifying creditors.

An AI-based loan and credit system can look into the behavior and patterns of customers with limited credit history to determine their creditworthiness. Also, the system sends warnings to banks about specific behaviors that may increase the chances of default. In short, such technologies are playing a key role in changing the future of consumer lending.

Tracking Market Trends

AI-ML in financial services helps banks to process large volumes of data and predict the latest market trends. Advanced mobile apps powered by machine learning in banking helps evaluate market sentiments and suggest investment options.

AI solutions for banking also suggest the best time to invest in stocks and warn when there is a potential risk. Due to its high data processing capacity, this emerging technology also helps speed up decision-making and makes trading convenient for banks and their clients.

Data Collection and Analysis

Banking and finance institutions record millions of transactions every single day. Since the volume of information generated is enormous, its collection and registration become overwhelming for employees. Structuring and recording such a huge amount of data without any error becomes impossible.

Innovative AI and banking software development company help in efficient data collection and analysis in such scenarios. This, in turn, improves the overall user experience. The information can also be used for detecting fraud or making credit decisions.

Customer Experience

Customers are constantly looking for better experiences and higher convenience. For example, ATMs were a success because customers could avail of essential services of depositing and withdrawing money even during the non-working hours of banks.

This level of convenience has only inspired more innovation. Customers can now open bank accounts from the comfort of their homes using their smartphones.

Integrating artificial intelligence in banking and finance services further enhances the consumer experience and increases the level of convenience for users. AI technology reduces the time taken to record Know Your Customer (KYC) information and eliminates errors. Additionally, new products and financial offers are released on time.

Eligibility for cases such as applying for a personal loan or credit gets automated using AI, which means clients can eliminate the hassle of manually going through the entire process. In addition, AI-based software reduces approval times for facilities such as loan disbursement.

AI in banking customer service also helps to accurately capture client information to set up accounts without any error, ensuring a smooth customer experience.

[Also Read: 6 ways Fintech industry is using AI to woo millennials]

Risk Management

External global factors such as currency fluctuations, natural disasters, or political unrest seriously impact the banking and financial industries. During such volatile times, taking business decisions extra cautiously is crucial. Generative AI services in banking offers analytics that gives a reasonably clear picture of what is to come and helps you stay prepared and make timely decisions.

AI for banking also helps find risky applications by evaluating the probability of a client failing to repay a loan. It predicts this future behavior by analyzing past behavioral patterns and smartphone data. Read the given blog to learn how technology is shaping the future of digital lending.

Regulatory Compliance

Banking is one of the highly regulated sectors of the economy worldwide. Governments use their regulatory authority to ensure that banking customers are not using banks to perpetrate financial crimes and that banks have acceptable risk profiles to avoid large-scale defaults.

Banks usually maintain an internal compliance team to deal with these problems, but these processes take a lot more time and require huge investments when done manually. The compliance regulations are also subject to frequent change, and banks need to update their processes and workflows following these regulations constantly.

AI and ML in banking use deep learning and NLP to read new compliance requirements for financial institutions and improve their decision-making process. Even though AI in the banking sector can’t replace compliance analysts, it can make their operations faster and more efficient.

Predictive Analytics

One of the most common use cases of AI in the banking industry includes general-purpose semantic and natural language applications and broadly applied predictive analytics. AI can detect specific patterns and correlations in the data, which traditional technology could not previously detect.

These patterns could indicate untapped sales opportunities, cross-sell opportunities, or even metrics around operational data, leading to a direct revenue impact.

Process Automation

Robotic process automation (RPA) algorithms increase operational efficiency and accuracy and reduce costs by automating time-consuming, repetitive tasks. This also allows users to focus on more complex processes requiring human involvement.

As of today, banking institutions successfully leverage RPA to boost transaction speed and increase efficiency. For example, JPMorgan Chase’s CoiN technology reviews documents and derives data from them much faster than humans can. Read the linked blog to learn how RPA is transforming the insurance sector.

Also Read: Digital Transformation in Banking: What it means for businesses

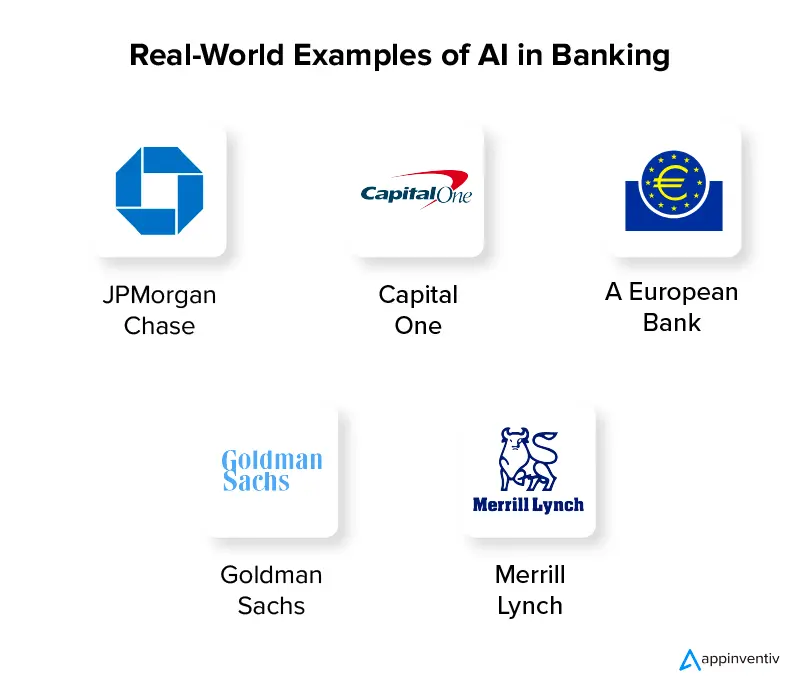

Real-World Examples of AI in Banking

As highlighted above, few big banks have already started leveraging artificial intelligence technologies to improve their quality of service, detect fraud and cybersecurity threats, and enhance customer experience.

Here are a few real-world examples of banking institutions utilizing AI to their full advantage.

JPMorgan Chase: Researchers at JPMorgan Chase have developed an early warning system using AI and deep learning techniques to detect malware, trojans, and phishing campaigns. Researchers say it takes around 101 days for a trojan to compromise company networks. The early warning system provides ample warning before the attack occurs. It also sends alerts to the bank’s cybersecurity team as hackers prepare to send malicious emails to employees to infect the network.

Capital One: Capital One’s Eno, the intelligent virtual assistant, is the best example of AI in personal banking. Besides Eno, Capital One also uses virtual card numbers to prevent credit card fraud. Meanwhile, they are working on computational creativity that trains computers to be creative and explainable.

A European Bank: Appinventiv worked with a leading European bank that wanted an AI-based solution to resolve customer queries in real-time. Within 10 weeks, the team deployed an AI-based chatbot assistant in the bank’s web and mobile apps capable of handling complex tasks such as resolving real-time customer complaints and reporting stolen credit card cases. With support for seven languages, the AI chatbot was ready to assist customers worldwide. This resulted in a 20% hike in customer retention.

Apart from commercial banks, several investment banks, such as Goldman Sachs and Merrill Lynch, have also integrated analytical AI-based tools in their routine operations. Many banks have also started utilizing Alphasense, an AI-based search engine that uses natural language processing to discover market trends and analyze keyword searches.

Also Read: Why are Banks Adopting Blockchain Technology?

Now that we have looked into the real-world examples of AI in banking let’s dive into the challenges for banks using this emerging technology.

Challenges in Adopting AI & ML in Banking

The wide implementation of high-end technology like AI is not without challenges. Several challenges exist for banks using AI technologies, from lacking credible and quality data to security issues.

So, without further ado, let’s take a look at them:

Data Security

The amount of data collected in the banking industry is huge and needs adequate security measures to avoid any breaches or violations. So, looking for the right technology partner who understands AI and banking well and offers various security options to ensure your customer data is appropriately handled is important.

Lack of Quality Data

Banks need structured and quality data for training and validation before deploying a full-scale AI-based banking solution. Quality data is required to ensure the algorithm applies to real-life situations.

Also, if data is not in a machine-readable format, it may lead to unexpected AI model behavior. So, banks accelerating toward the adoption of AI need to modify their data policies to mitigate all privacy and compliance risks.

Lack of Explainability

AI-based systems are widely applicable in decision-making processes as they eliminate errors and save time. However, they may follow biases learned from previous cases of poor human judgment. Minor inconsistencies in AI systems do not take much time to escalate and create large-scale problems, risking the bank’s reputation and functioning.

To avoid calamities, banks should offer an appropriate level of explainability for all decisions and recommendations presented by AI models. Banks need to understand, validate, and explain how the model makes decisions.

Why Must the Banking Sector Embrace the AI-First World?

Despite the current challenges, banks are in a race to become AI-first, and that too for a good reason. For many years, the banking industry has been transforming from a people-centric business to a customer-centric one. This shift has forced banks to take a more holistic approach to meet customers’ demands and expectations.

With their focus now on the customer, banks must begin thinking about how to serve them better. Customers now expect a bank to be there for them whenever they need it – which means being available 24 hours a day, 7 days a week – and they expect their bank to do it at scale.

To meet these customer expectations, banks must first overcome their internal challenges – legacy systems, data silos, asset quality, and limited budgets. The way banks can do this is with AI.

The Generative AI Impact

As these are just some of the issues that inhibit banks from moving quickly enough to keep up with their customer’s demands, it’s no wonder that many banks have turned toward AI as an enabler of this change.

Generative AI has also emerged as a robust solution to several of the challenges faced by banks today. By leveraging its ability to analyze and synthesize vast amounts of data, generative AI can streamline complex decision-making processes and enhance predictive analytics. This not only boosts efficiency but also significantly reduces operational risks associated with human error and oversight.

Furthermore, Generative AI use cases in banking include the creation of realistic synthetic data sets that help improve model training without compromising privacy. The technology can also generate automated, context-sensitive customer communications, complex financial reports, and regulatory documents in real-time, which are critical in maintaining compliance and enhancing customer service.

Applications of generative AI in banking go even further, particularly in developing sophisticated fraud detection systems. These systems are designed to adapt and learn from transaction patterns, significantly boosting security in a dynamic way. By embracing these applications, banks can effectively tackle operational challenges and transform how they engage with customers and handle risks, paving the way for a more secure and efficient banking ecosystem.

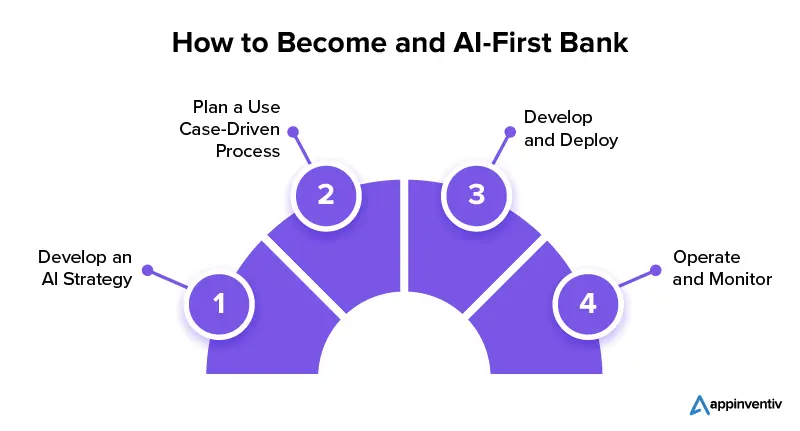

Steps to Become an AI-First Bank

Now that we have seen how AI is used in banking, in this section, we will look into the steps that banks can take to adopt AI on a broad scale and evolve their processes while paying due attention to the four critical factors — people, governance, process, and technology.

Step 1: Develop an AI Strategy

The AI implementation process starts with developing an enterprise-level AI strategy, keeping in mind the goals and values of the organization.

It’s crucial to conduct internal market research to find gaps among the people and processes that AI technology can fill. Make sure that AI strategy complies with industry standards and regulations. Banks can also evaluate the current international industry standards.

The final step in AI strategy formulation is to refine the internal practices and policies related to talent, data, infrastructure, and algorithms to provide clear directions and guidance for adopting AI across the bank’s various functional units.

Step 2: Plan a Use Case-Driven Process

The next step involves identifying the highest-value AI opportunities, aligning with the bank’s processes and strategies.

Banks must also evaluate the extent to which they need to implement AI banking solutions within their current or modified operational processes.

After identifying the potential AI in banking use cases, the QA team should run checks for testing feasibility. They must look into all aspects and identify the gaps for implementation. Based on their evaluation, they must select the most feasible cases.

The last step in the planning stage is to map out the AI talent. Banks require several experts, algorithm programmers, or data scientists to develop and implement AI solutions. They can outsource or collaborate with a technology provider if they lack in-house experts.

Step 3: Develop and Deploy

After planning, the next step for banks is to execute the process. Before developing a full-fledged AI system, they need to build prototypes to understand the shortcomings of the technology. To test the prototypes, banks must compile relevant data and feed it to the algorithm. The AI model trains and builds on this data; therefore, the data must be accurate.

Once the AI model is trained and ready, banks must test it to interpret the results. A trial like this will help the development team understand how the model will perform in the real world.

The last step is to deploy the trained model. Once deployed, production data starts pouring in. As more and more data starts coming in, banks can regularly improve and update the model.

Step 4: Operate and Monitor

The implementation of AI banking solutions requires continuous monitoring and calibration. Banks must design a review cycle to monitor and evaluate the AI model’s functioning comprehensively. This will, in turn, help banks manage cybersecurity threats and robust execution of operations.

The continuous flow of new data will affect the AI model at the operation stage. Therefore, banks should take appropriate measures to ensure the quality and fairness of the input data.

How Appinventiv Can Help in Your AI for Banking Journey

AI and banking go hand-in-hand because of the technology’s multiple benefits. As per McKinsey’s global AI survey report, 60% of financial services companies have implemented at least one AI capability to streamline the business process.

This indicates that the future of AI in banking is bright and promising. AI is set to revolutionize the banking landscape with the potential to streamline processes, reduce errors, and enhance customer experience. Thus, all banking institutions must invest in AI solutions to offer customers novel experiences and excellent services.

Being a leading artificial intelligence services company offering high-end FinTech software development services, Appinventiv works with banks and financial institutions to develop custom AI and ML-based models that help improve revenue, reduce costs, and mitigate risks in different departments.

Our IT consulting services experts can assist you in utilizing AI to generate transformational changes because of their knowledge of artificial intelligence and awareness of the particular problems encountered by the banking industry. They can help you create AI-powered solutions that enhance risk management, automate procedures, and improve client experiences.

Get in touch with our experts now to build and implement a long-term AI in banking strategy that caters to your needs in the most tech-friendly manner.

FAQs

Q. How does AI help in Banking?

A. AI for corporate banking automates tasks, boosts customer services through chatbots, detects fraud, optimizes investment, and predicts market trends. This increases productivity, lowers costs, and provides more individualized services.

Q. How AI helps in banking risk management?

A. Here are some ways in which AI in banking risk management helps prevent cyber attacks.

- Data analysis: AI systems analyze vast amounts of data to spot trends and abnormalities that could be signs of danger.

- Real-time monitoring: AI in digital banking keeps track of account activity and transaction data in real-time to quickly identify and address risks.

- Fraud detection: AI algorithms spot fraudulent actions by examining transactional data and customer behavior patterns.

- Compliance and regulatory requirements: AI helps banks ensure compliance with rules by automatically tracking transactions and producing reports.

- Predictive analytics: AI creates risk models and carries out predictive analytics to calculate the likelihood of defaults and market volatility.

Q. Which are the most important Generative AI use cases in banking?

Here are some of the most significant Generative AI use cases in banking:

Enhanced Fraud Detection: Generative AI models can simulate various fraudulent scenarios to improve detection algorithms, making fraud prevention systems more robust and responsive.

Risk Assessment and Credit Scoring: Generative AI is reshaping risk assessment and credit scoring in the banking sector. By creating detailed simulations of financial scenarios, generative AI tools provide deeper insights into credit risks. This helps the financial institutions improve the accuracy of their credit scoring models, leading to smarter lending decisions.

Document Processing Automation: Generative AI excels in automating the generation and processing of complex banking documents, reducing errors and increasing efficiency.

Personalized Customer Experience: Applications of generative AI in banking are pivotal in revolutionizing customer experiences. By leveraging generative AI, banks can analyze extensive customer data to craft personalized marketing campaigns that are aligned with individual customer preferences and behaviors, significantly enhancing the effectiveness of marketing efforts.

Q. What are the top AI trends in banking?

A. The impact of AI in banking is immense, which has made different banking and financial companies keep themselves updated with the recent trends:

- In banking, AI-powered chatbots and virtual assistants are being used to improve customer service, offer individualized support, and effectively handle common inquiries.

- RPA automates routine manual operations, like data input and document processing, boosting operational effectiveness and lowering banking procedure errors.

- By analyzing massive volumes of data, finding trends, and detecting fraudulent activities in real time, AI is increasingly utilized to identify and prevent fraud.

- With the help of AI, banks may use consumer information and preferences to provide individualized product suggestions, specialized offers, and specialized services.

- Owing to the massive advantages of AI in banking, FinTech companies are now investing in AI for banking that assists with complicated data analysis, market trend forecasting, and risk assessment, enabling more precise risk management and decision-making.

How Much Does it Cost to Build a Custom AI-based Accounting Software?

The accounting industry has been evolving very fast, and the expanding use of AI in accounting is becoming evident. According to The State of AI in Accounting Report 2024, 71% of accounting professionals believe that artificial intelligence in accounting is substantial. Considering the given number, it is easy to grasp why companies are keen on…

Generative AI in Manufacturing: 10 Popular Use-Cases

Introduction Manufacturing is truly getting a serious makeover for the future, and it's not full of buzzwords and techno-speak; with the dawning of AI technologies, manufacturing is no longer about nuts and bolts and conveyor belts. Yes! We are talking about how Generative AI in manufacturing is transforming the entire industry. It was the next…

10 Use Cases of Computer Vision in Manufacturing: What Revolution Can the Industry Expect?

The transformative phenomenon of Industry 4.0, born from the demands of resource and energy efficiency, urban production, and demographic changes, continues to shape the future of manufacturing. With its focus on automation, predictive maintenance, and process optimization, the digitalization phase brought in a new level of efficiency and responsiveness. And just when manufacturing units were…